It reminded me of March 20 when the global markets crashed on the apprehensions of coronavirus alleged to have been transmitted from Wuhan, China. Indexes alarmingly collapsed to lower levels and stocks sent shivers down the fragile spine of investors globally.

However, the brave souls who showed confidence and resilience in the financial markets were soon rewarded as the markets rebounded scaling new heights after a few months. Dow Jones, Nasdaq, Sensex, and all global indices not only retrieved their lost glories but also attained unprecedented levels.

Dow crossing 31000 and Nasdaq easing past 13000 levels was like leading from the front. The investors reposing confidence in the fundamentals having invested with due diligence were suitably rewarded as the stocks picked up during the pandemic multiplied their wealth multiple times.

Tesla, Amazon, Zoom in USA and Reliance, Bajaj Finance, TCS from India jumped to higher levels. Exactly after 11 months, we have witnessed another collapse again. It started from China and like a virus butchering the US, Australia, and Asian markets in no uncertain manner.

India following the Asian markets lost 1939 points on BSE and more than 500 points on Sensex. It was a double shock for Indian investors as many lost big money on Wednesday due to a glitch at the NSE resulting in interruption of business for more than four hours. Poor guys!! suffering losses for none of their faults. Huge losses accrued to the traders and today’s fall has added miseries to these investors again. US markets will be opening later tonight to decide the direction of global markets on Monday.

Bond yields to the extent of 1.61% have made the big investors exiting stock markets and preferring bonds for safe investment. This migration of funds will certainly impact the market sentiments. All markets will be watching Dow movements tonight and any good news will help recovery on Monday.

My genuine advice for the investors to maintain their composure and sit tight by selecting a few Cherry picks with cheaper valuation on the way. However, traders to sit on the sidelines for a few sessions and watch only the movements in this volatile turbulent market. Those who can’t resist the temptations must keep themselves covered by marking a stop loss to minimize the exposure. Avoid playing index and bet on the fundamentally strong stocks with lot of promise and potential. There are many in the market that you need to identify

Good luck! Friends

Success usually comes to those who are too busy to be looking for it….

Financial freedom generally denotes having resources, investments, and cash so that you can afford the kind of life you want. Individuals can take small steps each day towards this goal by following a budget and paying close attention to their finances.

How to move about?

Let’s find our way to Financial Freedom!! It’s not only your income but the habit of savings that make you financially independent. Don’t wait for your salary hike or scaling of the business. Just realise the significance and strength of small savings!! Regular savings of @10% per month can accumulate funds aggregating more than a month’s salary in your account in just 10 months? Not a big science only simple mathematics, you need to believe in yourself!

“You don’t have to see the whole staircase, just take the first step.”

Look back at your total salary last year? Were you not managing your life comfortably? You have already received your annual increment and maybe a promotion too, Right? Additional few dollars dropping in your Bank account has not made any difference except the frequency of dining out or buying a household item to improve your lifestyle. You have already exhausted by spending comfortably throughout the month and there is still a week to go when the next salary gets into your account?

How do people react ?:

This is what a decently employed person keeps doing till he confronts a serious problem of virtually no balance left in the account. He has to resort to quick high-cost borrowing for each and every activity involving money. This could be for hospitalization, child education, home repairs, loss of a job or any other emergency requirement.

#1. The only way to save is Auto Debit/Transfer:

Open another account with your bank and start saving by setting up auto debit instruction in your salary account today. This is the only and best way to avoid spending whatever you get in your Bank account.

For example, the net salary of Rs.50000/- is credited into your account on the 7th date of every month. An auto tranfer of 10% i.e Rs.5000/- will be automatically clicked on the same day leaving behind Rs.45000/- in your account. Hopefully, you will organize yourself to ensure all expenditute within the said amount.

#2 Set Up/Plan Your Budget:

No business, No state, No Country, and for that matter no family can survive without planning a budget. It’s a simple exercise of matching your likely expenses with the income/salary being credited in the Bank account every month. Though the living expenses remain on tips it is advisable to adopt a habit of writing in your diary every month. This will provide you an opportunity to have a look at the expenses for exploring chances of taking leverage on cutting down expenditure during a particular month.

“The goal isn’t more money. The goal is living life on your terms.” –Chris Brogan

Never allow your debt to surpass 10% of annual income; If your total annual salary/income comes out to be Rs.1200000/- then the short term debt should not go beyond 120000/- at any given time under any circumstances.

Earning and spending without having a clearly defined budget is like driving a vehicle carrying your family without knowing the destination and checking on the fuel required for your journey.

”If we command our wealth, we shall be rich and free. If our wealth commands us, we are poor indeed.”

– Edmund Burke

#3 Explore Extra Income Source:

The current pandemic condtions have made the world wiser and adaptable to the new environment as everything has kept moving though not as smooth as it should have been.

There is no dearth of finding an additional source of income that can supplement your resources for enjoying financial freedom. It depends on your resolve only that can initiate and identify utilizing the extra few hours at your disposal. This could be earning a few dollars by using your professional qualitifcation, hobbies by subscribing to the portals like freelancer, Udemy, and many others paying for the services on offer 24x7x365:

You can also explore the option of doing some online drop shipping business that doesn’t require you to maintain any inventory or account books. You can use your selling instincts by availing of marketing options to bring customers to your store. Leave everything from packing to the delivery upto the supplier. In the end, a handsome return to keep your retirement plan moving

Never miss an opportunity to use your credit card judiciously to earn points for earning cash backs or other such gifts by observing strict discipline.

Hi friends, do you have any other way of accomplishing financial freedom. Your feedback will be an enriching experience for me as well the readers. No one is a complete individual or professional in any field and I am not the exception.

your idle gold ornaments lying in the locker for years? Leave aside your emotional inhibitions and look for getting liquid cash within a few hours. It doesn’t require voluminous paperwork for satisfying your Bank either. You can carry the old/out of fashion and out of use gold jewelery to the nearest Bank or Gold Financing Company for a quick loan on easy terms in a few minutes.

Do You Need Urgent Money?

You have the easiest option of converting your idle gold ornaments lying in the locker for years into cash. Leave aside your emotional inhibitions and look for getting liquid cash within a few hours. It doesn’t require voluminous paperwork for satisfying your Bank either. You can carry the old/out of fashion and out of use gold jewelery to the nearest Bank or Gold Financing Company for a quick Gold loan on easy terms in a few minutes.

Is there any Maximum limit?

Every NBFC/Bank has its own prescribed policy for fixing the maximum and minimum loan exposure it usually ranges from Rs.1000/-to Rs.50 lakh. for a single customer. Muthoot Finance the leading player in Gold Loans has no upper limit: https://www.muthootfinance.com

How Much Will It Cost?

Gold Loan is a secured loan offered on a very affordable low-interest rates ranging from 7% to 19% depending upon the amount of loan and its repayment period. You can repay the loan along with interest in 36 installments, being the maximum permissible time limit. SBI has a customer-friendly gold loan scheme: https://www.sbi.co.in/web/personal-banking/loans/gold-loan

What will be the maximum eligibility?

RBI has a fixed LTV(Loan to Value) ratio of 90% meaning thereby that Banks can finance loans to the extent of 90% of your gold value that is derived from the average 22ct. gold Jewelry price prevailing in the market over the last 30 days. Maximum eligibility of loan amount depends on the weight of your gold ornaments which is multiplied by the per gam rates of the gold. Normally, Banks come up with a per gram rate on regular basis. Let’s take an example :

Weight of Your jewelry: 150gm; Rate fixed by the bank: Rs.3100/ per gram

Total eligibility of loan: 3100×150=Rs.465000/-

Can Gold Coins/Gold Biscuits also be pledged?

Please note that the RBI has not allowed loans against gold bullion i.e gold bricks, gold biscuits, etc. Banks will accept only gold ornaments for extending loan facility

How and Where to Go?

Though a number of companies have started online gold financing business, I will recommend you to visit any branch of the authorized Bank/Company in your vicinity for availing of the loan facility. Muthoot Finance, Mannapuram, IIFL, HDFC Bank, ICICI Bank, Federal Bank, and a host of other NBFC’s extending this facility have hundreds of branches to cater to the needs of customers. You can google for the nearest branch

What is the standard procedure:

Generally, all Banks/NBFC’s have a uniform operating system in place as appended below:

Carry documents, like, PAN Card, Aadhar Card, Passport, Bank account statement, and a canceled cheque for fulfilling the KYC norms.

You need to deliver gold ornaments to the authorized representative/BM for verifying the purity and quality of the gold. They have a prescribed laid down procedures to carry out this process in a few minutes’ time.

The ornaments are subjected to physical scrutiny and weight measurement in your presence. You will be briefed about the quality of gold and permissible loan amount with all terms of sanction.

Different parameters define the schemes floated by the companies. With the maximum eligible amount, you will be charged the highest slab of interest rate but with a minimum amount of loan, you will be paying the lowest interest rates. However, You can take a call depending upon your requirements and ease of repayment.

No complicated documentation!! It takes just a few minutes before the amount goes into your account

Wait for the message on your mobile phone for the credit entry in your account but don’t forget to collect a copy of the sanction letter specifying all details of the pledged gold ornaments and terms of sanction.

What about the safety of the Jewelry:

All the Banks/NBFC’s have a robust security system taking care of the safety norms. The pledged ornaments are sealed and signed before finding their way into the vault. No one except an authorized representative has access to the strong room where all the ornaments are stored. There is virtually no chance of any pilferage or mixing up the packets.

When do the companies auction ornaments?.

Your loan account needs to be adjusted by paying regular monthly installments. In case of any delinquency resulting due to non-payment of three installments, the account is treated as NPA(Non-Performing Asset) in compliance with RBI guidelines.

You will be reminded of your liability through personal calls, notices, registered notices, and finally, the gold will be auctioned as per the policy.

Who auctions the gold ornaments?

Auction: Though not a pleasant experience for gold ornaments occupying a specific emotional value in the hearts of every Indian, the lenders exercise their option of auctioning the pledged securities after exhausting all available avenues as under:

You will be informed at least 21 days before the date of auction preferably by a registered post on the last available address in the company records. You still have an option to get your ornaments released by visiting the concerned branch of the company at least one day before the auction.

Notice of auction will be carried out in the two local newspapers. One of the newspapers may be in vernacular language in which you have signed the documents

The company will conduct auction through independent, professional and Board approved auctioneers only

The company can not participate in the auction process but an authorized representative of the company will remain present during the process of the auctioning.

A complete record like date, time, venue, details of sales, details of bidders present, maximum bid amount, details of the maximum amount bidder in whose name the bid has been concluded shall be prepared for all audits and future verification by the regulator i.e RBI

Auction price per gram shall be in line with the gold jewelry prices on the preceding day subject to the quality of the pledged gold

The borrower/customer can participate in the auction and place his bid like any other bidder on the same terms and conditions.

Any balance of this auction proceeds is utilized to settle mandatory taxes and auctioneer’s commissions. It is a mandate agreement to comply with the Sales Tax Laws of the state where the auction is conducted

After carrying out the auction, the company will inform the customer about the total amount auctioned along with any other relevant details. The surplus amount, if any, after payment of a prescribed fee to the auctioneers, local taxes, and any other related expenditure, will be credited into the account of the customer.

The auction process will be made transparent as per the guidelines of “The association of gold loan companies for public auction(India)” under the overall prescribed RBI policy on gold loans,

image courtesy: bing.com

The Banks don’t insist for any declaration for end use of the loan amount sanctioned against the gold ornaments. You can use it for any purpose like investments, child education, payment of high cost debt, domestic ceremony or whatever you feel like. This is another simple way to repair your credit history.

Some of my friends from countries other than India might be surprised to find the entire post dedicated to the Indian conditions only. Yes, you are right! but believe me, all parameters are more or less the same in all the countries for availing gold loans by the customers. I can come back again on this topic if need be. Till then enjoy reading and keep me posted with your valuable feedbacks

All the traditional old stories attributed to financial advisors advocate for saving enough and controlling expenses being the only way to amassing wealth for a relaxed impending retired life in 20 to 30 years. The art of compounding keeps adding valuation to your investments at consistently good rates for the funds to grow on the expected graph.

Traditional instruments being Bonds, Mutual Funds, Bank Deposits, Shares will never eat into your entire capital as turbualence here and there may reduce the average returns only. The assets lying in your portfolio are safe, secure and easily accessible for encashmnt or swapping at any point of time.

We have seen over the past few decades that all the global indices grow at around 11 to 12% per annum. Leave aside the bubbles of markets crashes happening at irregular intervals causing anxieties in the minds of investors, the compounding factor brings a good wealth for you even if you stay invested passively. These are the strong plus points for those believing in safe and assured returns from their investments. Alas! this route of accumulation of wealth takes longer journey to your retirement at the age of 60 years.

However, for the possibility of your retirement occurring anywhere between 40 to 50 years of age, you will have to think differently!! The idea of putting your money in the most volatile and riskier options could be scary for the obvious reasons but we have been listening from the experts “More the risk- More the profit”. Your money will grow in proportion to your risk only.

The year end rally saw the cryptocurrency prices soaring sky high prompting me to contemplate allocating some money in this newly found love of cryptocurrency in general and Bitcoin/Etherium in particular. Though not a guaranteed return option yet an investment that can get you closer to your relaxed retirement sooner than planned. The risk to reward ratio is incredible as you will see in the following illustration.

Cryptocurrency has come a long way since the year 2010. From virtually nonexistant pricing, Bitcoin has touched $42000 recently. Bitcoin came into existence through its founder Santoshi Nakamoto in 2009 as the first blockchain-based cryptocurrency in the world. It was considered as an attempt to create an alternate arrangement for money transactions directly without using the usual authorized medium of Banks or financial institutions. Feeling threatened by the presence of cryptocurrency seemingly an alternate to the Fiat currency, all countries have remained in unacceptable mode to regulate this cryptocurrency so far.

The price of Bitcoin remained inconsequential for the initial few years but July 2010 saw this unregulated little-known currency moving up from $ 0.0008 to $0.08. A big jump by all means!! Did anybody ever contemplate investing in Bitcoin even in 2010? I think no one would have ever visualized that this scarce commodity will create a magic in few year’s time and investors will carry this currency to astronomical heights.

Despite some of the exchanges closing down due to intervention of the regulatory bodies in various countries, a sudden spurt in price transpired in 2013 when a bitcoin trading @$13 reached a maximum $220 by the end of the year. Bitcoin after attaining a mind-boggling price of $19780 in December 2017 cruised along with prices going down to the $3500 levels right through 2018 but bouncing back to five figures in 2019.

Starting from the third quarter of 2020, cryptocurrency market has shown a tremendous spurt in prices, and the level of $28000 for a bitcoin achieved in December looked invincible. But look at the way this currency has behaved right from the start of the current year. We have witnessed milestones after milestones getting crushed in every session as the price skyrocketed to $42000 a bitcoin levels in the first week of January 2021.

While there is a Maximum limit of Bitcoin i.e 21 million to be mined and 18.62 million have already been in circulation as of date. This limited supply has created the gap between demand and supply impelling the institutional investors to join the party in a big way. The news of more than 78% accessible bitcoins having been possessed by the institutional investors left retail investors vying for the remaining 22% available in the market. As anticipated, this continued demand-supply gap may swell the prices beyond the purview of small investors in the future.

Over the last ten years, this currency has grown from a meager $ 0.08 to $42000, growing to (42000 is a 52499900% increase of 0.08.) Unbelievable. An investment of 100 (roughly 1200 bitcoins) in 2010 would have become $50400000 as of the first week of January 2021. look at the table “A” below for more comprehension. Etherium, the number two altcoin in the market has also been showing tremendous growth in the company with its more illustrious elder brother Bitcoin. Etherium is the platform being used by a large number of small tokens in the market and is likely to remain in demand.

Name of Currency

Price 2010

Price 2015

Price 2020

Price 2021

Investment in 2010/15

Number of Bitcoin & value

Bitcoin

$0.08

$360

$28000

$42000

$100

1200=$50400000

Etherium

NA

$0.43

$753

$1393

$100

233=$324569

TABLE–A

Friends don’t you feel tempted to invest in this lucrative option despite being a risky proposition. To start with, let me put the various sentiments, both negative and positive about the future prospects of cryptocurrency in the words of leading businessmen/institutions to disseminate a fair idea before taking a dip in the crypto markets:

In the words of Warren Buffet, “I don’t have any Bitcoin. I don’t own any cryptocurrency, I never will,” he told CNBC in 2020. He has always been talking against this currency as these investments don’t follow the strictest terms of his legacy.

Another negative news on the volatility witnessed over the last few days as the UK regulatory has been quoted as saying :

“Individuals investing in crypto-currencies such as Bitcoin should be prepared to lose all their money, a United Kingdom regulatory agency warned. The Financial Conduct Authority (FCA) issued the warning after a sharp run-up in price in the last few months and a sharp decline over the weekend..https://moneywise.com/a/why-warren-buffett-hates-bitcoin

Slowly but surely most countries are opening up to cryptocurrency. We have regulated crypto exchanges like Coinbase, Bitflyer, Binance, Kraken, Huobi Global, etc to conduct business and a country like India has also started doing unprecedented business as all Banks allow transactions linked with cryptocurrency nowadays. I am not talking about the trading part which requires relevant skills and professionalism before jumping into this most volatile and risky business. However, this is an opportunity for those having a big risk appetite to venture into this portfolio for investing for a longer horizon.

The big brains of highly accredited professionals working with the leading Banks and Financial Institutions have been talking of a great future for this cryptocurrency.

US investment bank JP Morgan has created a crypto-currency to help settle payments between clients in its wholesale payments business. JPM Coin is the first digital currency to be backed by a major US bank. The crypto-currency, which runs on blockchain technology, has been used successfully to move money between the bank and a client account.

To conclude, I would love to present a very encouraging statement from the CEO of Pay-pal:

“I really like Bitcoin. I own Bitcoins. It’s a store of value, a distributed ledger. It’s also a good investment vehicle if you have an appetite for risk. But it won’t be a currency until volatility slows down.” —David Marcus, CEO of Paypal

Friends, looking at the briefly explained pros and cons of investing in this very tricky, speculative, and turbulent crypto market, you can take an informed decision before taking a call to venture into this unpredictable market. Short term players with fragile financial backup and a tendency to exit or enter the market frequently are prone to greater risk and must avoid spending restless nights after investments. However, as illustrated above, customers with high risk appetite may spare a few thousand to initiate into this market to reap rich dividends in the longer run.

What do you think of holding crypto currency in your portfolio as an alternate opportunity for a long term investment?

Stay Safe Stay Connected

Disclaimer: The material and information contained on this website/Blog is for general purposes only. You should not rely upon the material or information on the website as a basis for making any business, legal or any other decisions. Any reliance you place on such material is strictly at your own risk and responsibility

“If you don’t believe it or don’t get it, I don’t have the time to try to convince you, sorry.” – Satoshi Nakamoto

Free image: courtesy pixabay

Cryptocurrency or Bitcoin may be a atypical phraseology for an ordinary Indian citizen but you will be surprised to know that all the authorized exchanges in INDIA have recorded an extraordinary growth in the Cryptocurrency business since March 2020. Any conjecture amongst the investors or the Bankers has been removed by the Supreme court order dated 4th, March 2020, setting aside the circular issued by RBI in April 2018. Though no formal regulatory has been issued by the RBI for explicating the matter, the Banks/Customers/Exchanges have already started conducting the business.

There are pros and cons attributed to this unregulated currency but statements coming from the sources like Bill Gates creates confidence:

“Bitcoin is a technological tour de force.”– Bill Gates.

There has been an unprecedented increase in business over the last few months in India. The previous eight months starting from March 2020 till date have witnessed the growth of cryptocurrency business in India by more than 600%. Reportedly, the Indian cryptocurrency business with a monthly turnover of more than 23 million dollars stands at number 2 in Asia and number 6 in the world. Mind-blowing?

Launched in 2009 by an unknown person using the alias Santoshi Nakamato, Bitcoin is the new paperless currency that doesn’t have control by the Govts or Banks. It is a digital currency and you can not touch it with your hand. You can buy anything from hotel booking to furniture through this currency.

ATM’s and other dispensing centers facilitate convenient use of cryptocurrency by the customers in many countries. You can use your smart phone or computer to send or receive money without involvement of any Bank. The technology has brought a revolution in the Financial markets with more and more institutions coming out to provide commercial services to their customers.

Free image courtesy: pixabay

With a limited possibility of mining maximum 21 million of Bitcoins, the persistent demand of Bitcoin results in high volatility in the market. The market data suggests 18.75 million Bitcoins are already in circulation as of today. Big institutional investors have been amassing this coin continuously as the price is gradually moving beyond the reach of retail investors. The price of one Bitcoin has scrambled up from 8000$ to 27000$ within 12 months. That makes one Bitcoin equal to 27000×78= Rs.2079000 (Twenty Lac and seventy-nine thousand). Isn’t it a huge amount for one unit of Bitcoin? However, you can buy a small fraction of Bitcoin also.

Unlike, the currency notes and coins minted and printed by the Governments in the closely guarded printed press, these cryptocurrency coins can be mined by the miners from the convenience of their bed rooms. Highly sophisticated computers are used by the experts through a complicated “Blockchain” process popularly known as Mining. This being a technical and labour intensive exercise requires immense concentration. Anybody sitting at home can mine this currency and earn a value of 6.25 BTC for creating one block. By any standards, Its a huge compensation!!

The cryptocurrency markets are in operation 24x7x365 as the blockchain technology has made this market very competitive now. There are more than 6000 coins trading in the markets through hundreds of authorized cryptocurrency exchanges. Every coin has its distinct value and utility. Some of the most popular and traded coins in the markets are indicated below:

Bitcoin: BTC:

Etherium: ETH

Bitcoin Cash: BCH

Ripple: XRP

Litecoin: LTC

Binance: BNB

Cardano: ADA

Polkadot: DOT

Bitcoin SV: BSV

Steller: XLM

Free image courtesy pixabay

There are still many countries that have not regulated this currency for valid reasons and genuine apprehensions. Being a parallel economy without any control of the Central Bank or the Governments, this may land in the hands of terrorists or antinational activists. They have their own perceptions of losing the entire control over the currency and its regulatory authority. Most of the countries don’t want this to happen in their own interests.

From India’s perspective, strange statistics forewarn about the pattern of investors investing or trading in cryptocurrencies. More than 50% of investors in the crypto currency markets in India have an annual income of less than 10 lac.

This being a very risky volatile market with turbulences occurring at regular intervals, you must ensure to be circumspect and discreet in handling the transactions. Any impulsive act can make your money vanish in seconds. You can not approach your Bank or RBI for complaining about any pecuniary loss perpetrated by the swindlers through fishing and other fraudulant modus operandi.

Friends, Stay Safe Stay Connected but keep reading

Disclaimer: The material and information contained on this website/Blog is for general purposes only. You should not rely upon the material or information on the website as a basis for making any business, legal or any other decisions. Any reliance you place on such material is strictly at your own risk and responsibility

Personal Finance advisors never encourage frequent use of credit cards for good reasons. Many of us have spoiled our credit scores by spending recklessly ending up in debt beyond our means. We will take a look at whether the use of credit cards is prudent to satisfy our urgent instinct to buy everything that comes our way. Maybe a few important and relevant observations will enlighten your way for being more circumspect in using the credit cards in future.

Credit cards have some of the best features when it comes to better utilization. However, on the flip side delinquencies in payment of your liabilities can send you off the track easily sending nightmares of bad credit score.

image courtesy: bing.com

The possibility of an easily affordable credit requirement has made us comfortable when it comes to buying consumer goods or planning holidays. With the arrival of digital marketing, habits of saving first and then buying any household item has given way to compulsive buying.

Whether watching a movie, surfing the internet, or visiting any market place our purchasing instinct gets propagated to place an order immediately. The offers like zero interest installments, 1+1 free products, and other such freebies dolled out by the sellers send an illusion in our mind as if this product will not be available again on such prices again.

Strangely, Personal Loans, Credit cards, and a host of other easy credit options have made our job easier for nothing visibly going out of our wallet. Decisions for getting a Smartphone, new car, holidaying in distant foreign tourist destination, etc. have become instantaneous. Though all these credit options are more or less linked with your credit score the urge to keep ahead of your neighbor compels you to spend more than desired.

Though a strong believer in using a debit card instead of a credit card, I still feel comfortable using credit cards for the reasons explained below. A feel good element prompts me in maintaining clean payment records without falling into the traps laid by the credit card companies.

Positive Features:

Bonus: Any customer with an excellent credit score is enticed to opt for a new credit card with offers like one-time bonus, gift cards, full waiver of annual card renewal charges, or other such freebies. You must grab such offers maintaining strict discipline in utilizing your cards.

Rewards Points: Certain credit cards come with reward points which keep accumulating with every spending and you can exchange these points for the recharge cards, gift vouchers on the market platforms. Isn’t it worth considering?

Frequent Flyer Miles; Starting with American Airlines in ’80s, most of the companies have at least one such card in their kitty nowadays. You get a mile for every journey you undertake with the airline ticket purchased through this card.

Insurance. Credit cards come with inbuilt accident insurance under the master policy subscribed by the credit card companies.

Credit score Improvement: Better use of credit cards refixes your credit score for increasing future limits on the credit cards or going for a home loan later on.

TRAPS:

Coming to the Traps for those who are vulnerable and likely to default and damage credit score, these fallacious and confusing offers needs to be spurned:

image courtesy: bing.com

The first is about paying only the minimum of your bill. Believe me, it will take you months and years to finish paying off your credit card balance in full. The minimum payment requirement is only around 5% of your balance and other charges keep adding to your woes. If you want to significantly reduce your debts, you have to learn how to pay full amount of the bill rather than going easy on making the minimum payment.

Another trap is the late payment penalty where you are charged a late fee for even delaying payment by a few hours or even a day. Try to get these charges waived by talking to the companies as they have a tendency to waive off such charges for those customers who pay regularly.

Balance Transfer: This is modeled and promoted in such a way that the customer feels comfortable without realizing that his interest rate and annual renewal charges have been increased silently. This is just shifting of your liability and frequent use can trap you in debt.

Cash Withdrawals; Your credit card limit has a sub-limit of cash payments. Be careful of cash advances in credit cards. While this can help you during emergencies, it will be imposed with very high interest rates and transaction charges. If you cannot pay it back immediately, it can accumulate quite easily. Try to search for other options to finance your need. Credit card cash advances should be one of your very last options.

Please understand that cash withdrawals, Late payment charges, minimum payments or frequent balance transfers have an adverse impact on your credit discipline and history. Better avoid it!

Remedies for Debt Trapped Customers:

Never go for a settlement. It looks easy and convenient for settling your debt with credit card companies. Please note that credit card companies are very smart and don’t lose money. On the pretext of initiating legal proceedings for recovery of bad debts, they would have the option of adding legal expenses, late payment charges, and inflated interest accruals to demand an abnormally high amount from you. However, while settling your account, they will write-off these charges giving an impression of providing you a big relief. Before accepting such an offer you must negotiate with the company for waivement of charges instead of writing off a particular amount from your bill. Waivement doesn’t impact your credit history!!

Never Accept Write-off Offer: As explained above, the settlement of your bad debt is a bad option but allowing writing off the debt is worse than the settlement offer. Besides your actual bill, other charges will be included before writing off the whole amount. However, at any point of time in the future, you may be called upon to pay the whole written off amount for improving your credit score. Try to negotiate for payment of debt in easy installments by waiving of the interest/late payment or any other charges.

Conclusion:

Every cardholder enjoys an interest free credit for more than 30 days besides earning free gifts, cash rewards and frequent flyer miles. With desciplined utilization of cards, I think nobody except defaulter stands to lose anything by using credit cards. Don’t you feel gracious to have liquid money in your debit card for the whole month? How effortless it is to keep your credit score moving up by just avoiding the traps.

Partly or fully written-off proposals impairing your credit history must be avoided and instead negotiate for consolidation debt to raise a single debt to pay of multiple debts.

Advice:

Avoid missing payment of credit card bills by setting the payment on auto mode at least a day before the last day of the bill. Will it not be better if you schedule payment of the bill on the day of your salary? I will encourage you to buy all groceries and pay living expenses through credit card only. Whenever you feel an urge to buy anything other than living expenses, try to use the debit card. This will make you feel like falling back on the liquid money in your account and the proven human psychology will not allow you to spend from your reserves.

Wanna see money dropping into your accounts without working actively for earning this income? My friends, It’s not a fluke or sweepstakes!

I am talking about the Passive Income that helps you in living the lifestyle you had wished for right from the early years of your career. This is the income for which you toiled hard and planned meticulously for fulfilling a peaceful and relaxed retired life. In simple and straight words, I am going to enlighten your way to accomplish your dreams

Friends, there are hundreds of books and numerous blogs talking at length about this stream of income from different perspectives. They are engaged in feeding the unsatiated hunger of readers looking for a clue to their anxious inquiries about the income that doesn’t require you to work actively.

Reading a few books and surfing some leading blogs on Passive income, I could barely satisfy my inquisitive thirst for complete knowledge on the subject. Every blogger differed on one account or the other prompting me to reproduce those tested metrics which came through in my own life!! Yes, I will dwell upon the subject with my own personal experiences.

Entrepreneurship or a white-collar worker, eventually everyone tries to explore resources for increasing earnings to accumulate wealth that could generate income when we don’t work actively. Yes, I am talking of retirement!! A stream of income that drops into your account without working is better known as a passive income. Don’t we need passive income when we are not working?

Whereas we in India strive hard and continue working even after the statutory retirement age of 60 years, some developed countries have a tradition to retire early. This becomes achievable only when you are financially secured and all your financial obligations like children’s education, having your own home and a retirement fund are suitably covered. One of the most attractive characteristics of retirement is the freedom of living your life on your own terms.

This passive income is not another salary or traditional business profit from its operations but yet it’s not less than that. For salary and business profits, you have to work hard with your active participation but this income drops into our account without even moving out of the comforts of your bedroom. However, for earning this passive income, you need to make your money or your ideas work for you.

image courtesy: bing.com

The wealth amassed or capital gains accumulated over the years get you an income that does not require you to work actively. As a matter of fact, this stream of income is the only way to retire peacefully before or at the prescribed age of 60 years. The wealth created by you is not going to work while sitting in your Bank savings account due to meager returns. There are various options of investment where you can not only neutralize the inflation rates but also earn enough for living a good lifestyle.

Statistics indicate that a salaried person needs 70% of his last drawn salary for living the same lifestyle. It could be very convenient for those drawing pension from their employers as the payable pension constitutes 40 to 50%% of the last drawn salary leaving a gap of just 20% for comfortable sustenance. But those retiring without the privilege of pension may have to manage this income by investing their accumulated savings and capital gains in secured and better yielding investments.

Stocks: INVESTMENTS: With due respect to authors and bloggers, I beg to differ on treating investment in stocks as a passive income. Even the dividend stocks are not a source of secured passive income as it comes once or twice in a year depending upon the performance of a particular stock. At this stage of your life, You need a constant supply of income for your sustenance without eating into the corpus of wealth created over the years. At the best, this investment can help you in the creation of wealth for the average returns on stocks come around 10 to 14% per annum. I think wealth creation is a subject for consideration prior to your retirement and not now. Are you with me friends?

Mutual Fund: Most of the fund houses have schemes for paying monthly income on your investments. Dividends will vary depending on the performance of the fund. Though there is always a disclaimer by the Mutual funds that past distribution of dividends is not indicative for guaranteed future performance but You can identify any fund on the basis of its past performances and invest. Historically, every fund has been paying dividends of @10%. Handsome returns!!

Certificate of Deposits: Though not popular in India even after more than 20 years of its existence, this instrument is available with most of the Banks and issued for a specific period on premium interest rates.

Bank FDR: A most liquid option that can be encashed any time as per your requirement. Though comparatively returns are on the lower side but this is like a balance having both characteristics of earning and liquidity. The inflation rates are easily neutralized

Rental Income: This is the best source of passive income as the real estate keeps appreciating over the years and simultaneously giving you a regular stream of rental income. You can invest directly in the property or through the REIT (Real Estate Investment Fund) to avoid cumbersome activities like, maintenance of the property, leasing formalities, recovery of rent, or vacating the property involving litigations.

Bonds: Normally these are the secured and tax-free high yield instruments that you can invest in for longer horizons. You don’t have to pay taxes as well, the regular payments keep coming into your account

P2P Lending: Though a bit riskier investments but it has a lot of potential for earning a regular income. The default rate is minimal in developed countries but in India too this regulated platform is maturing by every day. More than 40 P2P lending websites are operating in India promising great returns to the investors and convenient short-term lending to the start-ups.

Blogs/YouTube Channels: Though getting more competitive and tougher these days but establishing information products through blog/ebooks and youtube channels is one of the best ways to generate income by sitting at home. You can create your own video channel and sell-through Udemy, Skillshare, and Coursera platforms. It doesn’t cost you anything but once clicked there is a tremendous opportunity of earning

Drop Shipping: You have a niche for marketing and selling products? this is the best way of earning money while sitting at home. You are not required to maintain stocks by renting out premises or godowns. Right from packing, delivery, and confirmation, everything is done by the supplier. Identify one or two products by establishing your own platform on Shopify or Etsy. Import hundreds of products through the tools available. Spread the word through mouth or google, and popularise the product. Google business helps you free of cost in finding new customers. Customers interested in your product will visit your store and buy the product by paying online. The money will land into your account as a difference between the cost and selling price. By any means, this is handsome income!

image courtesy: bing.com

Conclusion: You have just found the easiest ways to generate passive income involving a little effort on your part. These methods have been practically experienced by me and found worthwhile with virtually no risk to the capital.

I will encourage you to start looking for passive income, a few years before you actually want to retire. With passive income you can have money coming in even as you pursue your primary job or business without interruption.

The prevailing pandemic conditions caused due to COVID 19 have resulted in economic upheavals rendering millions of people jobless. Those who had explored the opportunites of passive income earlier in their careers must have been able to fend for themselves in a more prudent way than others.

Hi Friends, Are you with me on the definition and interpretation of passive income. I will look for your valuable inputs for enriching my experience. Here is a link to Chris Hogan post on passive income that I would like you to read

Millions of Indians have been contributing in the financial growth of more than 200 countries spread over all the inhabited continents. It is not only for earning their livelihood, but the Skilled/Nonskilled, Businessmen and agriculturists also play a great role in the economic activities of these countries. Some of these are first generations who migrated from India and others maybe those who were born and brought up outside India by their parents or grandparents.

Image courtesy: bing.com

A sense of belongingness reverbrates in their blood arteries through the genes as every person of Indian origin nurtures a desire to keep India , the native land close to his heart. They have been exploring India by visiting places for tourism, religious or domestic ceremonies from time to time. We feel pride in watching a large number of India born young IT Professionals leading the top Multinational companies with their sheer hard work and competitive brilliance.

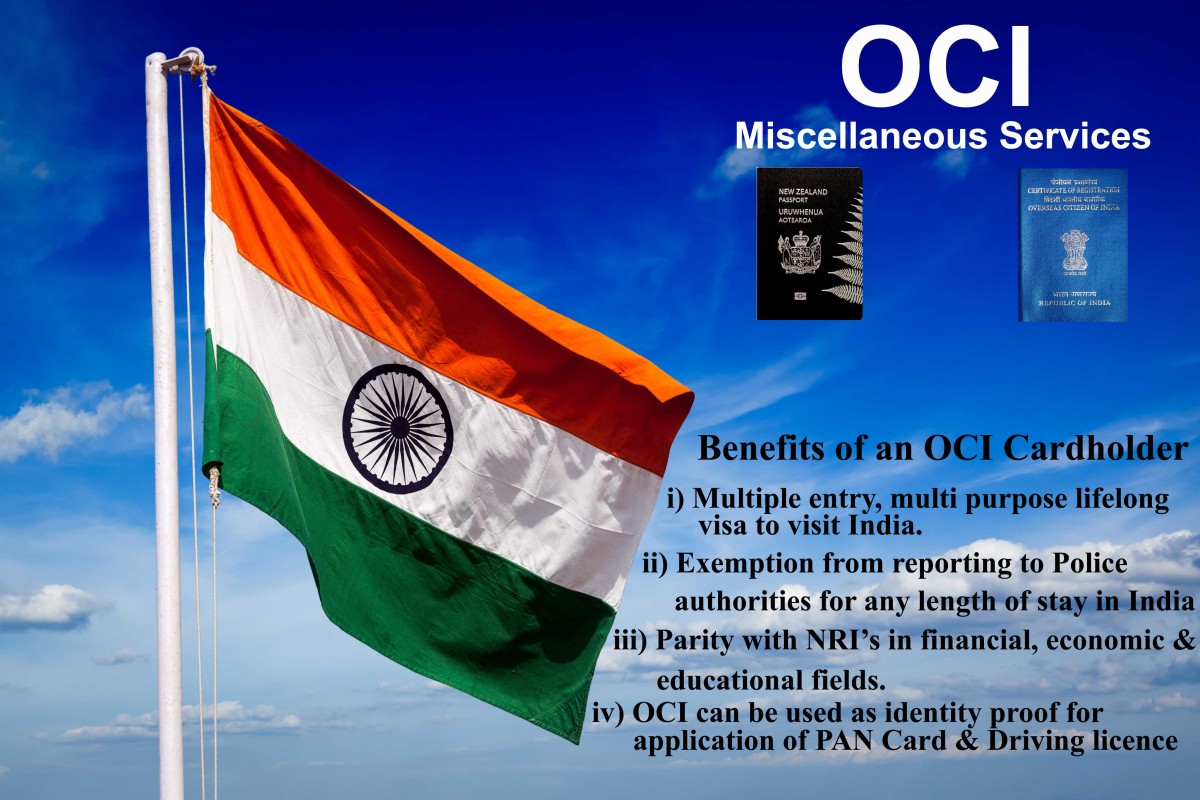

Though the Indian Government does not believe in extending dual citizenship for anyone holding overseas passports they have provided an alternative for all Indians who have surrendered their Indian passports for acquiring overseas citizenship. We are going to have an extensive view of how to apply for an OCI card, the privileges, and responsibilities identified with OCI cards now being issued to the Indian settled abroad.

NRI vs OCI: There is a distinct variance between NRI’s and OCI’s as by definition every NRI remains an Indian for all practical purposes like voting rights/getting Govt. employment in India /Buying or selling of property including agricultural land in India. All such privileges continue till they surrender their Indian Passports for becoming foreign nationals. On the other hand, OCI’s are foreign nationals who held Indian passports in the past or their parents/grandparents/ancestors were citizens of India.

Who is an OCI: Any foreign national who has migrated from India for permanent settlement abroad by surrendering an Indian passport to acquire overseas citizenship is termed as an OCI/PIO. This could be first-generation immigration or identified through their ancestors who were citizens of India as per the constitution 1950. OCI terminology appeared in 2005. However, those enjoying the status of PIO (Persons of Indian Origin) were merged into the OCI(Overseas Citizens of Inda) category in 2014. They were given the option to apply for the issuance of an OCI card free of cost.

Eligibility: (i) you must be an Indian born or citizen of India in terms of citizenship act 1950(ii) your parents or grandparents were citizens of India (iii) you are a foreign national spouse of an Indian citizen

Prescribed Fee; Applying from within India: $210 or Rs.15000/-; Applying from outside India: $275

How to Apply: Online; However after registering online by submitting pdf files of relevant documents and images of the applicant as well as signatures images, an application form with a specific number will be generated. You need to submit this duly completed and signed application form with documents and prescribed fee to the nearest Indian Mission/consulate for the necessary processing

Documents: Original surrender certificate issued in lieu of surrendering your Indian passport on acquiring overseas passport/citizenship. Proof of relationship to be produced by foreign nationals who are applying on the basis of their parents/grandparents being Indian citizens. Original foreign Passport with a minimum validity of six months at the time of application. Birth Certificate and certificate of naturalization in case of the USA nationals, Signatures, and two photos of the applicant.

Img.courtesy : bing.com

Time Taken: Normally 60 days time is taken for issuance of OCI card to the applicants. Application received by the Indian consulate is sent to Indian authorities who in turn issue the card and send it to the Indian Consulate for delivery to the applicant.

Status of PIO card Holders: They have been given the option for converting to OCI card free of cost

Where to apply: ociservices.gov.in Foreign nationals can not apply for OCI cards in India if they are traveling on a tourist visa or any other type of temporary visa

Validity: Normally OCI card is issued for a lifetime and the holders can stay in India without bothering to reissue of visa. However, a person under the age of 20 years needs to get his/her OCI card renewed on every renewal of the passport. No such renewal is required for those in the age group of 21 to 50 years, However, those crossing age of 50 years need to get their OCI card and visa reissued only for one time.

Revoking: You have to be very careful in your conduct abiding by the Indian laws, as a small local altercation violating the law could prompt the authorities revoking this card

What you can do: (i) You can stay in India permanently (ii) you can do business in India(iii) You have been placed at par with NRI’s as far as financial privileges are concerned.

Privileges: Multiple entry, multiple purpose lifelong visa to visit India. No more requirement to report to Police for staying any number of years in India. OCI card can be used as an Identity proof for the purposes of Pan Card application or DL in India

What you can’t do: Neither, You can buy agricultural land, nor enter active politics in India. Though there is no bar on getting employment in the private sector, Government jobs are beyond the purview of OCI card holders.

PAN Card: Yes, PAN is required for conducting certain transactions like, purchase of a car, house, shares, mutual funds, etc. An OCI cardholder can apply for the issuance of a PAN card online using form 49AA and making payment of a prescribed fee of Rs..864(Eight Hundred and Sixty Four) plus GST only. Once the payment is accepted, the application should be downloaded and signed before sending it to the issuing office along with the required documents. The PAN card will be issued and sent to your overseas address. Link to the websites for application: (https://www.pan.utiitsl.com/PAN/index.jsp) and https://tin.tin.nsdl.com/pan/index.html)

Bank Accounts and Home Loans: The OCI cardholders are at par with the NRI’s and can open accounts with the Banks, remit funds to their friends/relatives, and avail home loans as per their eligibility and entitlement.

Exceptional countries: Foreign nationals belonging to Pakistan, Bangladesh, Iran, Afghanistan, Sri Lanka, Nepal, Bhutan are not allowed to apply for OCI cards.

Grievance Redressal Cells: All Banks have an NRI cell for redressal of their complaints and providing support pertaining to the transactions in their accounts. Some of the states have dedicated special cells for registration of police complaints against fraudulent acts threatening their properties back home

Friends, I have tried to cover every aspect of features associated with OCI and their rights in comparison with the NRI’s in a precise and simple words but there is every likelihood having missed many relevant facts to be included in this post inadvertently. Your valued feedback will help in providing more researched knowledge in future posts.

Stay safe and keep reading

Disclaimer: The material and information contained on this website/Blog is for general purposes only. You should not rely upon the material or information on the website as a basis for making any business, legal or any other decisions. Any reliance you place on such material is strictly at your own risk and responsibility

We normally find Gold, Stocks and Real Estate moving in different directions. Loss of one could be a gain for the other. There are certain factors contributing to this peculiar ball game in the investment options. Staying strong and taking the world out of the mayhem caused by the Coronavirus pandemic conditions across the globe, we are fortunate to see the whole economy slowly emerging out of the dark tunnel of uncertainties. Even while the vaccination process has already commenced in a number of countries, corona cases have suddenly shown a soaring curve causing anguish but the economic activities have not stopped. Looks encouraging!! The world has learned how to live with Corona, this unwanted unwelcomed intruder in our life.

Global markets crashed in March 2020 showing no remorse to the small investors but the crippled world somehow managed to keep moving with a few sectors finding the time of their life as the sales turnover zoomed. Lockdowns and confinement of people within the boundary walls of their houses, left them trying various options to remain busy. Whereas, the entertainment and travel-related industries suffered, there was a piece of good news for online platforms, consumers, media, Pharma, and communication industries as the consumption of internet data increased.

The pernicious Corona started its venomous bite in Feb. 2020, as the following images illustrate the sudden impact on Gold and Stock markets in the USA. Dow crashed to 20900 levels after achieving the unprecedented highs of 29000 earlier and gold showed nervousness at $1566 levels on 28th Feb 2020.

Whereas, the Dow Zone has spiraled up to unprecedented 31000 levels, the International Gold @$1566 per ounce in Feb 2020 has consolidated to $1880 levels today after peaking to levels of $2067 during the year 2020.

Photo by Jose Francisco Fernandez Saura on Pexels.com

The Indian markets were no different as the nervousness lit large everywhere. Sudden lockdown forced lakhs of workers with meager belongings on their heads walking hundreds of miles to reach their native villages. It was a heart-burning scenario for the people watching their countrymen subjected to inconvenience in the absence of proper transportation and lack of cohesion between the state and the federal government.

Indian gold prices tumbled due to very low demand from domestic customers. However, Gold prices at Rs.43200 per 10 gm in Feb 20 has also shown prominence by moving up to Rs.49300 per 10 gm as of today after touching the historical highs of 52400 in November 2020.

Moving with the International sentiments, Nifty slipping down to unbelievable levels of 8000 in March 2020 has recovered smartly to unprecedented levels of 14595 as of today. Smart investors have made tons of money by investing at the right time when everyone was exiting the markets in panic and desperation. Nifty 50 trading at around 7600 in March 2020 has doubled the money in less than a year. Your self belief, courage, confidence, preseverance never goes wasted when it comes to investments.

During these turbulent times, we saw the concept of three avenues of investments never going hand in hand as they form parallel lines in the global economies without any exception. The three options of investments being Real Estate, Gold, and Stock Markets. The money keeps oscillating between these three strongest pillars of the economy. The liquidity pushed stock markets higher being the convenient way of entering and exiting any time while sitting at home. On the other side, the purchase of property, and physical gold proved cumbersome exercise.

Gold, Stock Market, and Real Estate never move in tandem. While the quality stocks kept moving the stock markets, the big players ploughed money into gold as the best remedy of uncertainty in turbulent times. Despite infusion of funds and consumer-friendly policies devised by the Government, there were no takers for investing in real estate during the year 2020. Hundreds and thousands of built or partially built apartments are standing unsold for the lack of interest, by the end-users. However, with the consolidation of gold prices, the demand looks picking up in real estate now.

With stock markets, and gold prices going through the roof, the best options lie in Real Estate now. Valuations of quality stocks have reached a point of consolidation and gold prices are also stabilising after achieving 25% growth in one year only. Right pockets may be explored for picking up rental or commercial properties for eyeing on the passive income.

Friends, the basic principle behind every investment is to create wealth by earning good returns from the investments regularly. Early retirement is possible only if you accumulate enough wealth for you to afford your current lifestyle. Believe me, a timely investment in real estate/stock market/gold can help in creation of wealth to earn passive income later on.

During the past ten years the gold prices in India have gone up from Rs.18000/- per 10 gm. to Rs.50000/-. Nifty(Stock Market) has gone up from 6134 levels on 31/12/2010 to 14595 today. Real Estate has also given tremendous returns over the last ten years.

Conclusion: What are you thinking about dear friends? Try to understand the movements of these three pillars of the economy by correlating the circumstances as stated above and invest at the right time in the right option.

Expense Ratio is the cost which every investor has to be best while investing in Mutual Funds and other related products. Before going deep into the relevance and calculation of this ratio, I would like to brief you about these very safe and income generating investments for you to comprehend the subject: Definition of Mutual Fund:

In simple words, Mutual funds invest in Multiple instruments with money pooled from many investors to invest across a spectrum of securities. Mutual Funds invest in various types of securities like Shares, Bonds, Govt Securities, Commercial Papers, etc. Mutual Fund is considered one of the most viable investment option for all types of income groups as it offers attractive returns to the investors. It does not require introduction of very large amount of funds but a nominal amount as small as Rs.500/-would be sufficient to start with. SIP is the most preferred option for investment by small investors in India. You can purchase any number of Mutual Fund units online at a daily arrived NAV(Net Asset Value) directly from the AMC.

Investors can pick any fund as per their goals and risk appetite. An Equity Fund could be riskier but yields higher returns, whereas a Debt Fund with Gilt Edged securities may be fully secure offering low returns. Historical data indicates an average return of +10% for investments with a minimum horizon of 5 years. Considering that all the funds are managed by highly qualified Fund Managers/Professionals, there is virtually no scope of losing your capital by investing in Mutual Funds.

With the passage of time, these traditional Mutual Funds have taken different forms to satiate the ever-increasing thirst of investors for augmenting their returns with maximum ease and diverse exposure depending on their risk appetite. Index Funds/ETF(Exchange Traded Funds), Fund of Funds, etc are the few most preferrable.

Index Fund:

Whereas the Mutual Fund invests in shares/securities and tracks individual investment daily, Index Fund is a mutual fund which the fund manager tracks with a particular index like S&P 500, Nifty50, ASX200, Dow 30, Nasdaq 100, Russel 2000. The Fund Manager prefers to invest in the bucket of securities held in the index implying an average return to the customers/investors at par with the Index only. If the Nifty 50 has gone up by 10% over the last two months, then the investors who invested in the Nifty 50 index will also get a return of app 10%.

index fund img: Courtesy bing.com

(Exchange Traded Funds) ETF:

ETFs are similar to mutual funds or index funds except that the Mutual funds can be bought or sold from the companies directly at the day end prices but ETFs are traded throughout the day like shares and can be traded any time of the day during the working hours of the stock market. ETFs generally hold stocks of commodities like Gold, Oil, Shares, Bonds, Currencies, etc.

ETF Fund image: Courtesy bing.com

Fund of Funds:

These funds have a large scope of providing multi-index spread over nulti-markets and countries to their customers. An investor living in India has an option to invest in International stocks like Amazon, Apple and Tesla by subscribing to these funds. Fundamentally, Fund of Funds is an investment strategy of holding a portfolio of other funds rather than buying individual stock and other securities. In simple terms, these Funds will buy other funds in their portfolios.

Hopefully, you have understood and comprehended the definition of mutual funds and their potential returns that may help you in identifying the right product for your investment. Let’s come to the subject i.e TER (Total Expense Ratio) that impacts the returns accruing to all the mutual fund investors.

Nothing comes free in this world! For that matter, no service comes free as there are always declared or concealed charges which you have to pay for utilizing those services. Despite no entry no exit charges on Mutual Funds, we have evolved a terminology known as Expense Ratio which is used by the AMCs to charge the investors. All costs of managing the funds are recovered from the investors at the time of exit. This cost comprises the management fee, brokerages, selling and marketing expenses, commissions, and other related expenditure.

Let us see how this TER is calculated and impacts a customer who has invested his money in any scheme of the mutual fund. A company(AMC) with an AUM of Rs.50000 crores earns a profit of 14% from its operations and as per SEBI guidelines, this company is supposed to charge TER @0.80%. The customer will get returns of 16%-0.80%=13.20%.

Management Fee: Almost all the Mutual Funds are managed by Fund Managers who are highly qualified professionals. Whatever salaries or contract amount is paid to the fund managers is booked under this head of expenses

Administrative Costs: Various charges such as brokerage, register, and transfer fee, legal and audit fee, advertising and, marketing costs, etc contribute as administrative expenses

Distribution Fee: Most of the schemes are marketed and sold by the mutual fund distributors approved and enlisted by the AMFI/NSE, etc A fixed rate of trail commission is paid to these distributors

If we sum up all these expenses and divide it by total assets of a particular Fund, the resultant value will be the Expense Ratio. Simple?

TER img: Courtesy bing.com

As per the SEBI circular, the under noted TER slab rates have been approved for all AMCs for meticulous compliance. SEBI has authorised certain exceptions that may cause a difference between two similar Mutual Funds. The investors need to compare the expense ratio of a company with other investment companies to ascertain whether this is worthy of investment or not A small difference in expense ratio can cause a considerable variation in your returns.

Assets Under Management(AUM)

TER for Equity Oriented Schemes

All other schemes excluding ETF/Index Fund

Index Funds

ETF Funds

Rs.500 crores

2.25%

2.00%

Next Rs.250 Cr

2.00%

1.75%

Next Rs.1250 cr

1.75%

1.50%

Next Rs.3000 Cr

1.60%

1.35%

Next Rs.5000 cr

1.50%

1.25%

On the next Rs.40000 cr

Total expense ratio exemption of 05% for every Rs.5000 cr

Total expense ratio exemption of 05% for every Rs.5000 cr

Above Rs.50000 cr

1.05%

0.80%

0.50%

0.35%

Total Expense Ratio(TER) as applicable in India

Friends, there is a distinct deviation in Expense Ratio between Equity/Debt and ETF mutual fund schemes. You will appreciate that equity fund involves 24×7 commitment and involvement of Fund managers for selling buying the securities by participating in all the trading sessions. This requires a lot of expertise, brokerage charges, and other connected expenses to be incurred by the Mutual Fund companies. Comparatively debt funds, index funds and ETF require minimal efforts as the entire process being passive in nature is less expensive. Hence the divergence in the Expense Ratio !!

However, the SEBI has allowed the AMCs to determine their own Expense Ratio based on the above chart and some relaxations as under:

For marketing and selling of mutual fund schemes beyond the top 30 cities across India, the AMCs have been allowed to charge 30 basis points .e 0.30 % of the fee in addition to the above-mentioned structure.

In the name of exit load AMCs have been allowed to include 0.05% in their TER

Where to find the TER(Total Expense Ratio): It’s very convenient to find out the Expense Ratio of any Mutual Fund Scheme either by accessing the relevant data available on the website of the concerned AMC or from the following sources:

Fund’s prospectus if you are already a customer

Financial News websites

AMFI

Though Expense ratio keeps changing in all the countries but it ranges in between 1 to 2% on actively managed funds and less than 0.20% on passively managed funds.

The USA, being the most developed and mature economy, expense ratio in actively managed funds like equity fund is less than 0.58% and it is .07% in passively managed funds. In ETF funds it was being charged at .03%

Conclusion: you will appreciate that the Expense Ratio as explained above is the actual cost incurred by the AMCs in managing these big Funds. The investors have suddenly diverted their investments in the newly found love of ETFs as the expense ratio is just a fraction. Friends, the Assets Under Management (AUM) of Indian Mutual Fund Industry as on November 30, 2020 has crossed a landmark of Rs. 20 Lakh crore and stood at ₹30,00,904 crore. The AUM of the Indian MF Industry has grown from ₹ 6.65 trillion as on November 30, 2010 to ₹30.01 trillion as on November 30, 2020 about 4 ½ fold increase in a span of 10 years. From this given data, you can visualize the reasons of expense ratio going down in India over the last few years.

Disclaimer: The material and information contained on this website/Blog is for general purposes only. You should not rely upon the material or information on the website as a basis for making any business, legal or any other decisions. Any reliance you place on such material is strictly at your own risk and responsibilityDisclaimer: The material and information contained on this website/Blog is for general purposes only. You should not rely upon the material or information on the website as a basis for making any business, legal or any other decisions. Any reliance you place on such material is strictly at your own risk and responsibility